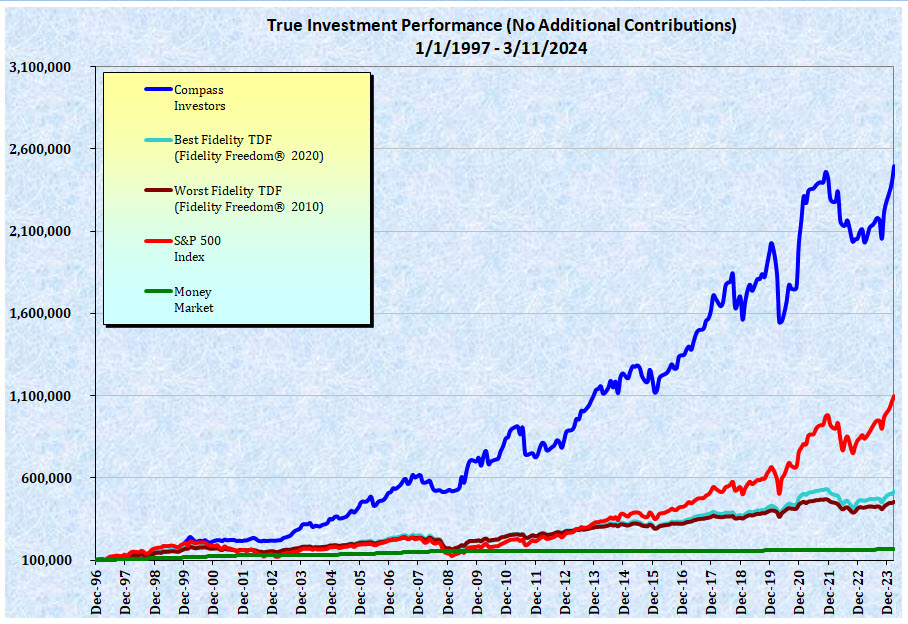

We offer a 90-day trial period to

first-time subscribers. The trial includes up to three Action

Reports, along with full access to the

instructions and tools needed to align your investments with

your best-positioned fund choices. We invite you to study

our archives of past Model Portfolio allocations and go

through our easy-to-follow Reallocation Process to see for

yourself just how straight-forward it really is. You may

cancel at anytime during the first 90-days for a full

refund.

30-Day Money Back Guarantee

There are no long-term contracts or commitments. You may

cancel for any reason within the first 30 days of any

billing for a no-questions asked full refund.

Loyalty Pricing Guarantee

For as long as you remain a subscriber, your yearly renewal cost will never increase.

Move your move over the yellow-box, right click, and select 'Always Allow Pop-ups from This Site...' from the displayed list of choices. , then follow the steps:

Move your move over the yellow-box, right click, and select 'Always Allow Pop-ups from This Site...' from the displayed list of choices. , then follow the steps:

{kind=link}